Guidecrypto exchange maker taker feesmaker vs taker fees explainedlowest fee crypto exchanges 2026crypto trading fee comparisonreduce crypto trading feeszero fee crypto exchangebest crypto exchanges for tradingcrypto spot vs futures feescrypto order types explained

Maker vs Taker Fees: 7 Crypto Exchanges Compared (2026)

Maker vs taker fees compared across Binance, Kraken, MEXC, Bybit, OKX, dYdX and Hyperliquid. Breakeven formulas, VIP tiers, and the EV decay formula that kills sub-20 bps scalping edges.

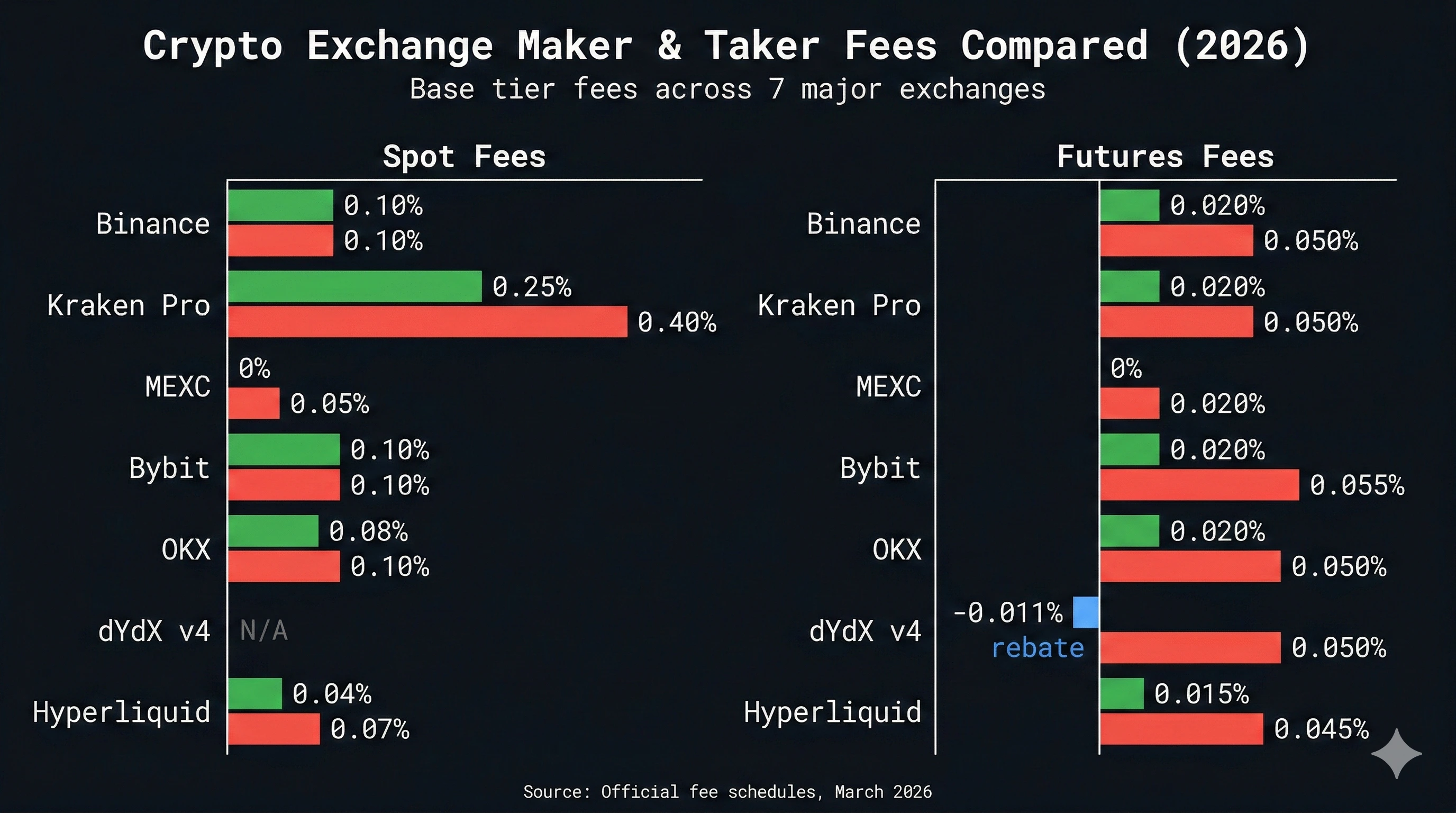

Crypto Exchange Maker Taker Fees Compared (2026)

\n\n| Exchange | Best For | Spot Maker / Taker | Futures Maker / Taker | Fee Discount |

|---|---|---|---|---|

| Bitget | Competitive perp maker fees + BGB discount | 0.10% / 0.10% | 0.020% / 0.060% | 20% with BGB |

| Binance ⭐ | Overall liquidity | 0.10% / 0.10% | 0.02% / 0.05% | 25% BNB (spot), 10% BNB (futures) |

| Kraken Pro | EU / institutional | 0.25% / 0.40% | 0.02% / 0.05% | Volume tiers to 0% maker |

| MEXC | Altcoin scalping | 0% / 0.05% | 0% / 0.02% | 50% with 500 MX tokens |

| Bybit | Derivatives trading | 0.10% / 0.10% | 0.02% / 0.055% | VIP tiers + MNT token |

| OKX | Unified margin | 0.08% / 0.10% | 0.02% / 0.05% | OKB tiers, VIP 5 = 0% maker |

| dYdX v4 | Decentralized perps | N/A | -0.011% / 0.05% | DYDX staking + Surge 50% rebates |

| Hyperliquid | DEX perps | 0.04% / 0.07% | 0.015% / 0.045% | HYPE staking up to 40% off |

A 5 Basis Point Fee Turned My Profitable System Into a Money Loser

\n\nLast year, I built a momentum scalping algorithm targeting 15 basis points of gross profit per trade on BTCUSDT perpetual futures. It had a 60% win rate across 3,000 backtested trades. On paper, the expected value was +3.0 bps per trade—a consistent grinder.

\n\nThen I ran it live with taker orders at 5 bps per side. The round-trip fee ate 10 bps out of every trade. My +3.0 bps edge became -7.0 bps. After 200 trades, I'd lost $1,400 in fees alone. The system wasn't broken—the fee structure was.

\n\nThat experience is why this guide exists. Most fee comparison articles dump numbers into a table and call it a day. This one treats fees as a mathematical engineering problem. You'll learn the exact breakeven formulas for long and short positions, see how Expected Value decay destroys scalping systems, and understand why a "cheap" exchange might actually cost you more than an "expensive" one once you account for spreads, slippage, and funding rates.

\n\nI've routed hundreds of automated trades through Binance's API, tested MEXC for altcoin scalping, and used Kraken Pro's SEPA Instant rails from Slovenia for EUR deposits that settle in seconds. Every fee number in this guide has been verified against official exchange documentation as of March 2026.

\n\n \n

\nWhy Trust This Guide and How We Evaluated Fees

\n\nThis guide evaluates crypto exchange fees through direct testing, not screenshots from marketing pages. Every fee tier was verified against official fee schedules as of March 2026.

\n\nOur methodology weighs four dimensions: explicit fees (maker/taker percentages), implicit costs (spread, slippage, market impact), fee optimization paths (VIP tiers, token discounts, staking), and total cost of ownership (including funding rates for perpetual futures positions). I personally trade on Binance, Kraken, and MEXC, and I've tested Bybit, OKX, dYdX, and Hyperliquid through funded accounts.

\n\nThree things this guide provides that most competitor guides don't: exact breakeven price formulas that account for fee compounding on notional value, the Expected Value decay calculation that shows when fees flip a winning system into a loser, and an honest assessment of implicit costs on thin altcoin order books (where the spread alone can exceed the maker fee by 10x).

\n\nWhat Are Maker and Taker Fees in Crypto Trading?

\n\nMaker and taker fees are the two-sided pricing model that crypto exchanges use to charge for trades. Makers add resting orders to the order book and pay lower fees (or earn rebates). Takers execute against resting orders, removing liquidity, and pay higher fees. The classification depends on whether your order executes immediately, not on the order type you select.

\n\nThis distinction exists because exchanges need deep, liquid order books to attract volume. If nobody rests limit orders at various price levels, there's nothing for incoming market orders to match against. The spread widens, slippage increases, and the exchange becomes unusable for serious trading. So exchanges penalize liquidity removal (taker) and subsidize liquidity provision (maker).

\n\nHow Does a Maker Order Work?

\n\nA maker order is any order that does not find an immediate match when it reaches the matching engine. It gets posted to the central limit order book (CLOB), where it rests passively until another trader aggresses against it. The maker provides a valuable service: deepening the book and narrowing the effective spread.

\n\nThe risk you take as a maker is adverse selection. Your resting bid at $59,900 is essentially a free put option for the rest of the market. If flash crash news drops Bitcoin to $55,000, your order fills at $59,900 milliseconds before the price collapses. The lower maker fee (or rebate) is direct compensation for bearing this risk.

\n\n\n\nHow Does a Taker Order Work?

\n\nA taker order matches instantly against resting liquidity. All market orders are taker orders by definition—they instruct the matching engine to fill at the best available price, sweeping through the book until the full size is executed. Limit orders that cross the spread also become taker orders.

\n\nTakers pay a premium for two things: speed and certainty. When you need to exit a position during a cascading liquidation event, waiting for your limit order to fill isn't an option. The extra 3-5 bps in taker fees buys you guaranteed execution.

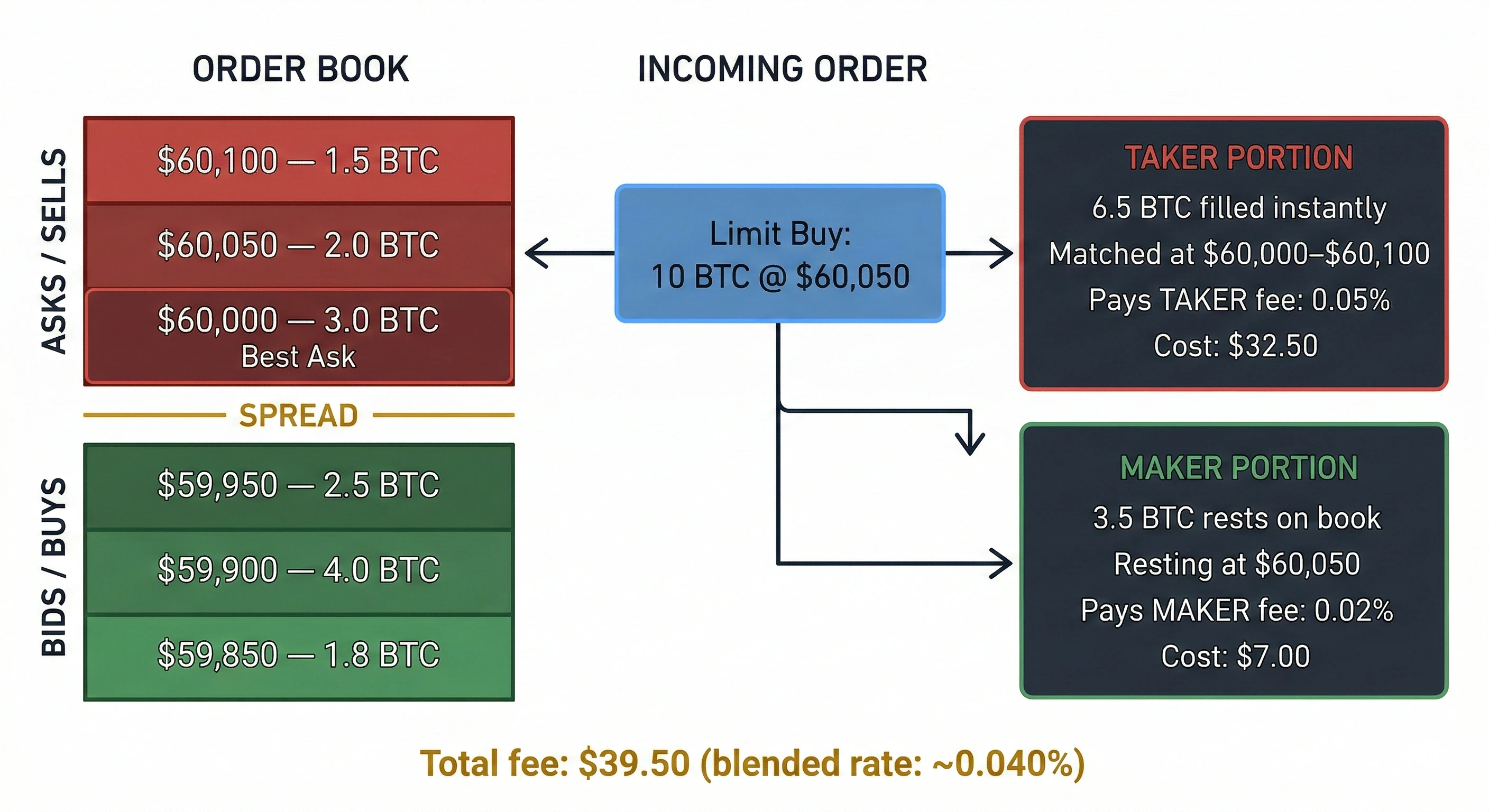

\n\nWhat Happens with Partial Fills?

\n\nLarge orders can receive split fee classifications. If you submit a 10 BTC limit buy that partially crosses the spread, the portion matching immediately is charged taker fees. The remaining unfilled amount rests on the book and, when eventually matched by another trader, is charged maker fees. This is why institutional desks use VWAP and TWAP algorithms—they parse partial fill probabilities to minimize aggregate costs.

\n\n \n

\nNow that you understand how the matching engine classifies orders, the next question is: how do you control which fee you pay? That's where advanced order types come in.

\n\nWhich Order Types Guarantee Lower Fees?

\n\nAdvanced order types let you control fee classification with precision. The Post-Only directive, IOC, FOK, and iceberg orders each serve different roles in fee optimization and execution management. Understanding them is the difference between paying 2 bps and paying 5 bps per side.

\n\nThe Post-Only Directive: Your Fee Insurance Policy

\n\nA Post-Only order tells the exchange: "Only accept this order if it will rest on the book. If it would cross the spread, cancel it instead." This is the single most important order type for fee optimization. Available on Binance, Bybit, Kraken, OKX, dYdX, and Hyperliquid.

\n\nI use Post-Only on every automated entry in my trading systems. When the spread is volatile and your limit price might momentarily cross, Post-Only prevents accidental taker fills that wreck your cost basis. For scalping strategies where the entire edge is 5-15 bps, one accidental taker fill can erase the profit from three winning trades.

\n\nIOC, FOK, and Iceberg Orders

\n\nImmediate-or-Cancel (IOC) orders fill whatever portion they can at the limit price immediately, then cancel the rest. Every executed portion is strictly a taker transaction—the unfilled part never rests on the book.

\n\nFill-or-Kill (FOK) orders demand complete execution of the full size at the specified price. If the book can't absorb the entire order, it cancels completely. Also exclusively taker. A common mistake: traders assume FOK orders are maker orders because they're limit orders. They're not—if they execute at all, they consume existing liquidity.

\n\nIceberg orders slice large positions into smaller visible tranches. As one tranche fills, the next appears. Since each tranche rests on the book, iceberg orders consistently accrue maker fees while hiding total position size from other participants.

\n\n\n\nStop-Market vs Stop-Limit: The Fee Trap

\n\nStop-Market orders trigger a market order when the price crosses your stop level. They guarantee execution but guarantee taker fees and, in thin liquidity, severe slippage during cascading liquidation events.

\n\nStop-Limit orders trigger a limit order instead. If you set the limit price away from the spread (stop at $60,000, limit sell at $60,100), the order rests on the book as a maker. The tradeoff: if the market gaps through your limit price, the stop-loss never fills and you're exposed to unbounded downside.

\n\nUnderstanding order mechanics is half the equation. The other half is recognizing that the maker/taker fee printed on your exchange's fee page is only one component of your total execution cost. Let's break down the full picture.

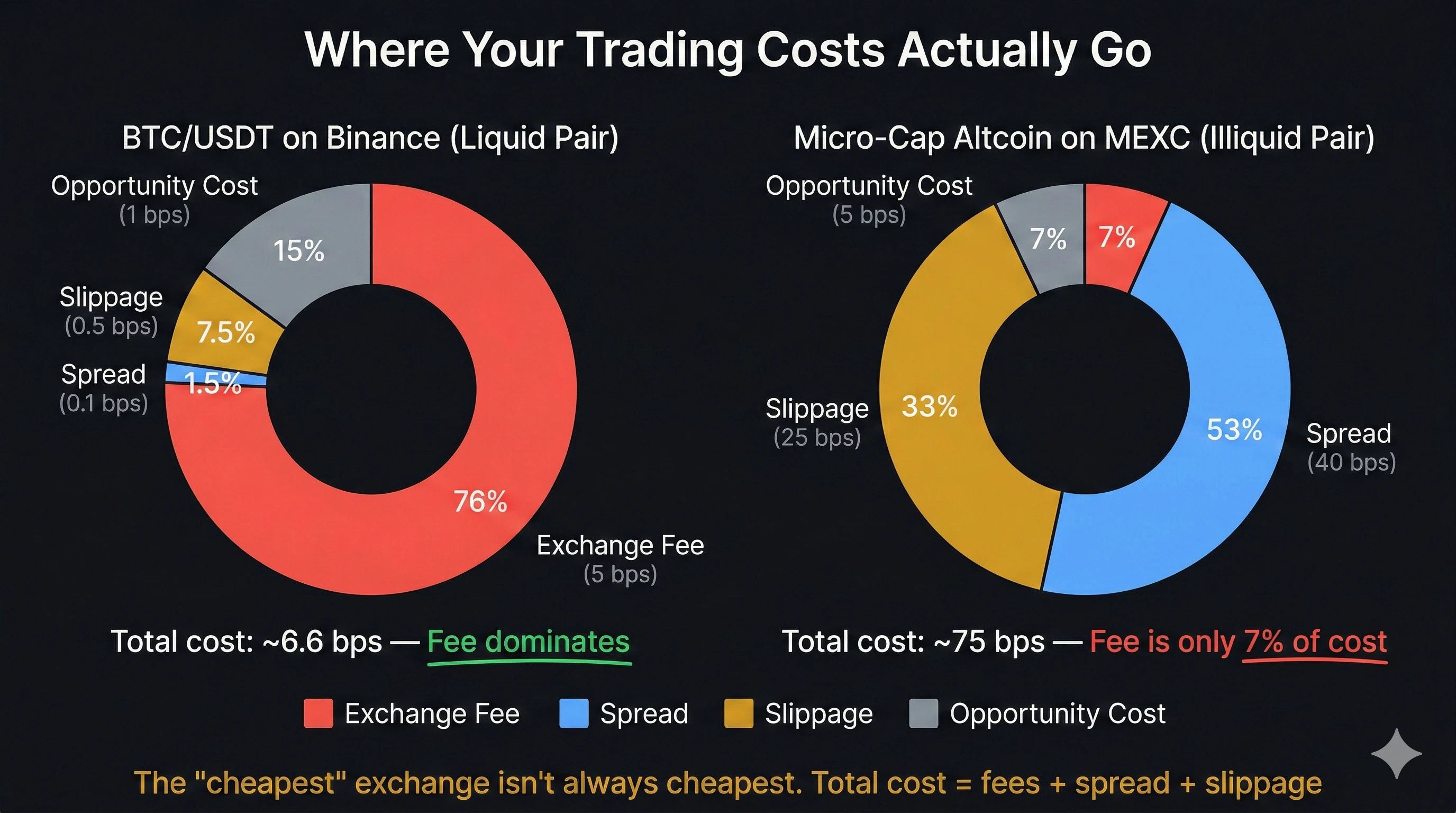

\n\nWhat Is the True Cost of a Crypto Trade?

\n\nTransaction cost analysis (TCA) measures the gap between the price you intended to trade at and the price you actually received. The exchange fee is the most visible cost, but it's frequently the smallest. Spread, slippage, and opportunity cost often dwarf the explicit fee—especially on illiquid pairs.

\n\nExplicit Costs vs Implicit Costs

\n\nExplicit costs are deterministic charges: the maker/taker percentage, flat withdrawal fees, and on-chain gas (for DEXs). You see them on your trade confirmation.

\n\nImplicit costs are structural drags that arise from market microstructure:

\n\nBid-ask spread: When you take liquidity, you cross the spread. On BTC/USDT on Binance, the spread is often 0.1 bps or less. On a micro-cap altcoin, it can exceed 50-100 bps. That's a hidden cost equivalent to 5-10x the explicit taker fee.

\n\nMarket impact (slippage): When your order is larger than the resting liquidity at the best price, the matching engine fills deeper into the book. Slippage scales non-linearly with order size.

\n\nOpportunity cost: For makers, this is the profit forfeited when the market moves away from your resting limit price and you never get filled.

\n\n \n

\nWhen Paying Taker Fees Is the Right Move

\n\nStandard advice says "always use limit orders." But TCA reveals scenarios where paying the taker premium is mathematically optimal.

\n\nIf your model predicts a 200 bps breakout in the next 30 seconds, resting a Post-Only limit order to save 3 bps risks missing a 200 bps gain. The opportunity cost vastly exceeds the fee. Similarly, during a cascading liquidation waterfall, getting out at taker fees plus 5 bps slippage beats waiting for a limit fill while the price drops another 300 bps.

\n\nThe math is simple: pay taker fees when the expected opportunity cost of non-execution exceeds the fee differential. For 90% of trades, maker orders are optimal. For the critical 10%, taker execution is a risk-management necessity.

\n\nNow let's put exact numbers on how fees affect profitability. These formulas are what separate informed traders from the ones who wonder why their "winning" system loses money.

\n\nHow Do You Calculate Breakeven Price With Trading Fees?

\n\nThe breakeven price is the exact exit price where your net profit is zero after all fees. These formulas account for the fact that fees are charged on the notional value, which changes between entry and exit as the price moves.

\n\nBasis Points and Notional Cost

\n\nFees in institutional crypto are measured in basis points (bps): 1 bps = 0.01% = 0.0001 as a decimal. A 5 bps fee on $100,000 notional = $50. With leverage, this matters: a $10,000 margin position at 10x creates $100,000 notional exposure. The $50 fee is a 0.5% hit against your $10,000 margin—not 0.05%.

\n\nLong Position Breakeven Formula

\n\nP_exit = P_entry × (1 + F_entry) / (1 - F_exit)

\n\nExample: You enter long at $100,000 with 0.04% taker fee on both legs.

\nP_exit = $100,000 × 1.0004 / 0.9996 = $100,080.03

\nBitcoin needs to move $80 (8 bps) just to break even. On a 10x leveraged position with $10,000 margin, that $80 move is a 0.8% drawdown before you earn a single dollar.

\n\nShort Position Breakeven Formula

\n\nP_exit = P_entry × (1 - F_entry) / (1 + F_exit)

\n\nExample: Short at $100,000 with 0.04% round-trip taker fees.

\nP_exit = $100,000 × 0.9996 / 1.0004 = $99,920.03

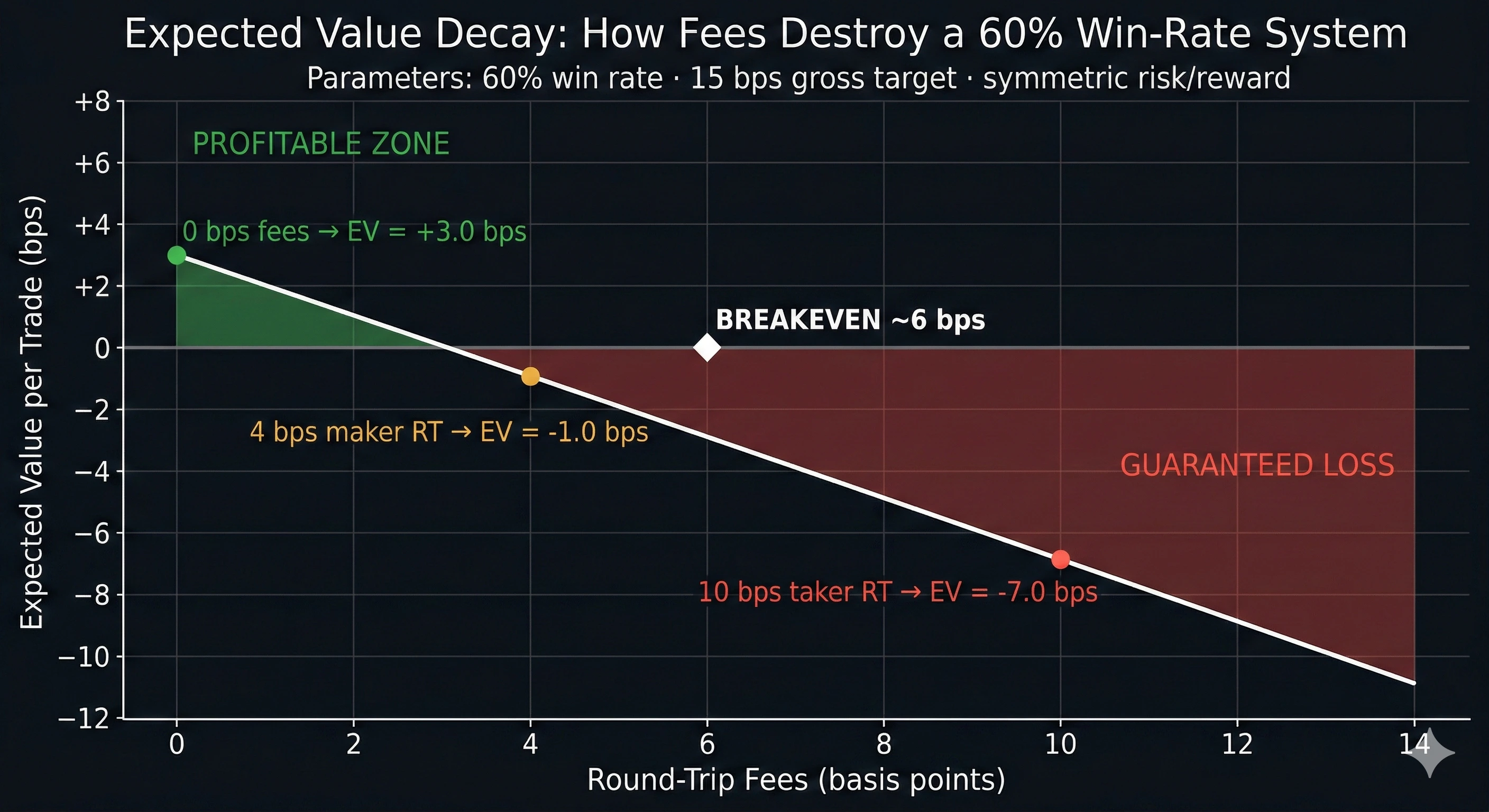

\n\nThe Expected Value Decay Formula: When Fees Destroy Your Edge

\n\nThis is the most important section in this guide. Consider a momentum scalping algorithm with these parameters:

\n\nWin rate: 60%. Average gross win: 15 bps. Average gross loss: 15 bps (symmetric).

\n\nWithout fees: EV = (0.60 × 15) - (0.40 × 15) = +3.0 bps per trade

\n\nWith 5 bps taker fees (10 bps round-trip):

\nNet win = 15 - 10 = +5 bps. Net loss = -(15 + 10) = -25 bps.

\nNew EV = (0.60 × 5) - (0.40 × 25) = 3.0 - 10.0 = -7.0 bps per trade

\n\nA 5 bps taker fee transforms a profitable system into guaranteed capital destruction. After 1,000 trades on $100,000 notional, that's a $7,000 loss from fees alone.

\n\n\n\nNow, if you switch to Post-Only maker orders at 2 bps per side (4 bps round-trip):

\nNet win = 15 - 4 = +11 bps. Net loss = -(15 + 4) = -19 bps.

\nNew EV = (0.60 × 11) - (0.40 × 19) = 6.6 - 7.6 = -1.0 bps per trade

\n\nBetter, but still negative. Now on MEXC with 0% maker fees (0 bps round-trip for maker-to-maker):

\nEV = (0.60 × 15) - (0.40 × 15) = +3.0 bps per trade

\n\nThe same system goes from -$7,000 to +$3,000 purely by changing the exchange and order type. That's the engineering variable.

\n\n \n

\nWith the math established, let's evaluate each exchange on what matters: explicit fees, VIP optimization paths, and real-world cost for active traders.

\n\n#1. Binance — Best Overall for Liquidity and Fee Optimization

\n\n\n\nWhy We Chose Binance

\n\nBinance consistently offers the deepest order books in crypto. After routing hundreds of automated trades through their WebSocket API, I can confirm that BTC/USDT spread is typically under 0.1 bps during active hours, and the order book absorbs $1M+ market orders with minimal impact. For futures, the 0.02% maker / 0.05% taker base fee is competitive, and the 10% BNB discount drops taker to an effective 0.045%.

\n\nThe VIP tier system rewards volume aggressively. At VIP 9 ($5 billion+ monthly volume), futures maker fees drop to 0% and taker to 0.017%. Even VIP 1 ($1M volume + 25 BNB) provides meaningful savings. For algorithmic traders, the API rate limits are generous and the WebSocket feeds deliver microsecond-precision order book updates.

\n\nWhere Binance particularly excels is infrastructure reliability. I've had my data collection systems running continuous WebSocket connections for months with near-zero disconnections. The matching engine handles extreme volatility events without the 5-10 second freezes I've experienced on smaller exchanges.

\n\nBinance Fee Schedule — Key Tiers

\n\n| Tier | 30d Volume (USD) | BNB Required | Spot Maker/Taker | Futures Maker/Taker |

|---|---|---|---|---|

| Regular | <$1M | 0 | 0.10% / 0.10% | 0.02% / 0.05% |

| VIP 1 | ≥$1M | 25 | 0.09% / 0.10% | 0.016% / 0.04% |

| VIP 3 | ≥$20M | 250 | 0.06% / 0.07% | 0.014% / 0.032% |

| VIP 5 | ≥$150M | 1,000 | 0.025% / 0.031% | 0.012% / 0.024% |

| VIP 9 | ≥$5B | 11,000 | 0.012% / 0.024% | 0% / 0.017% |

Source: Binance Official Fee Schedule, verified March 2026.

\n\nBNB discount: 25% off spot fees and 10% off futures fees when paying with BNB. Enable this in Settings → Fee Level → toggle BNB deduction. Keep a small BNB balance in your spot wallet.

\n\nPros and Cons

\n\n\n\n\n

\n\nPros

\n- \n

- Deepest order books globally—BTC/USDT spread consistently under $1 \n

- Futures fees among the lowest at base tier (0.02% / 0.05%) \n

- VIP 9 offers 0% maker on futures—genuine institutional pricing \n

- 25% BNB discount on spot is easy to activate \n

- API infrastructure is battle-tested and highly reliable \n

- Widest range of futures pairs (300+) \n

Cons

\n- \n

- Not available to US residents (Binance.US is a separate, limited entity) \n

- VIP tier requirements are steep—VIP 3 needs $20M monthly volume AND 250 BNB \n

- Regulatory uncertainty in multiple jurisdictions (EU, UK, Japan) \n

- Customer support response times can stretch to 48+ hours for non-VIP users \n

Pricing

\n\n\n\n \n\n

\n\n#2. Kraken Pro — Best for EU Traders and Institutional Compliance

\n\nWhy We Chose Kraken Pro

\nKraken Pro is the exchange I use for EUR deposits. From my Slovenian bank account, SEPA Instant deposits arrive in my Kraken account in under 30 seconds.

\nThe spot fee structure starts higher than Binance at 0.25% maker / 0.40% taker, but the volume tiers are more attainable.

\nFor high-volume institutional traders ($10M+ monthly), Kraken's fee schedule becomes genuinely competitive.

\n \n\n

\n\n#3. MEXC — Lowest Base Fees for Altcoin Scalpers

\n\nWhy We Chose MEXC

\nMEXC's fee structure is, on paper, unbeatable: 0% maker on both spot and futures.

\n \n\n

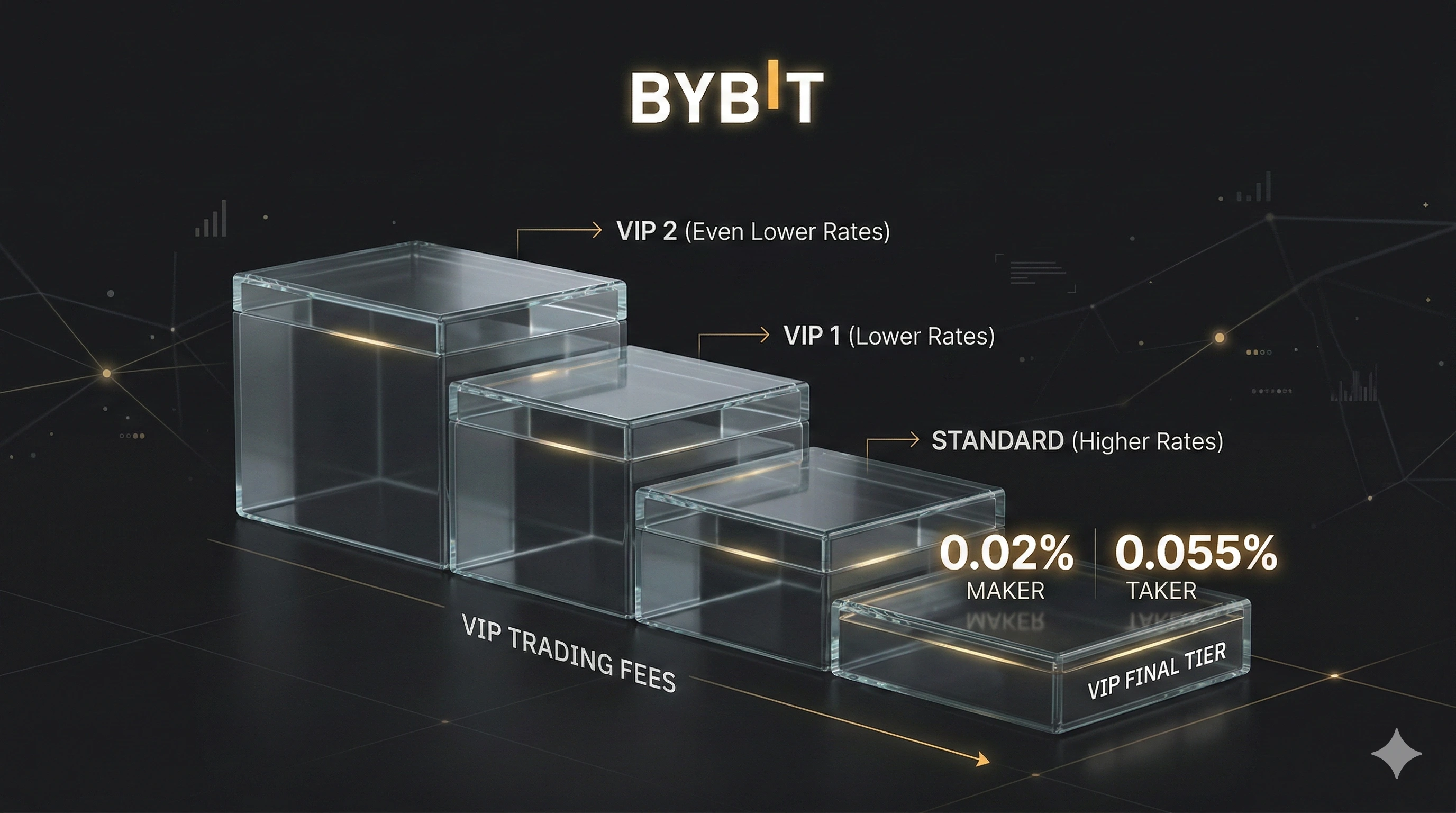

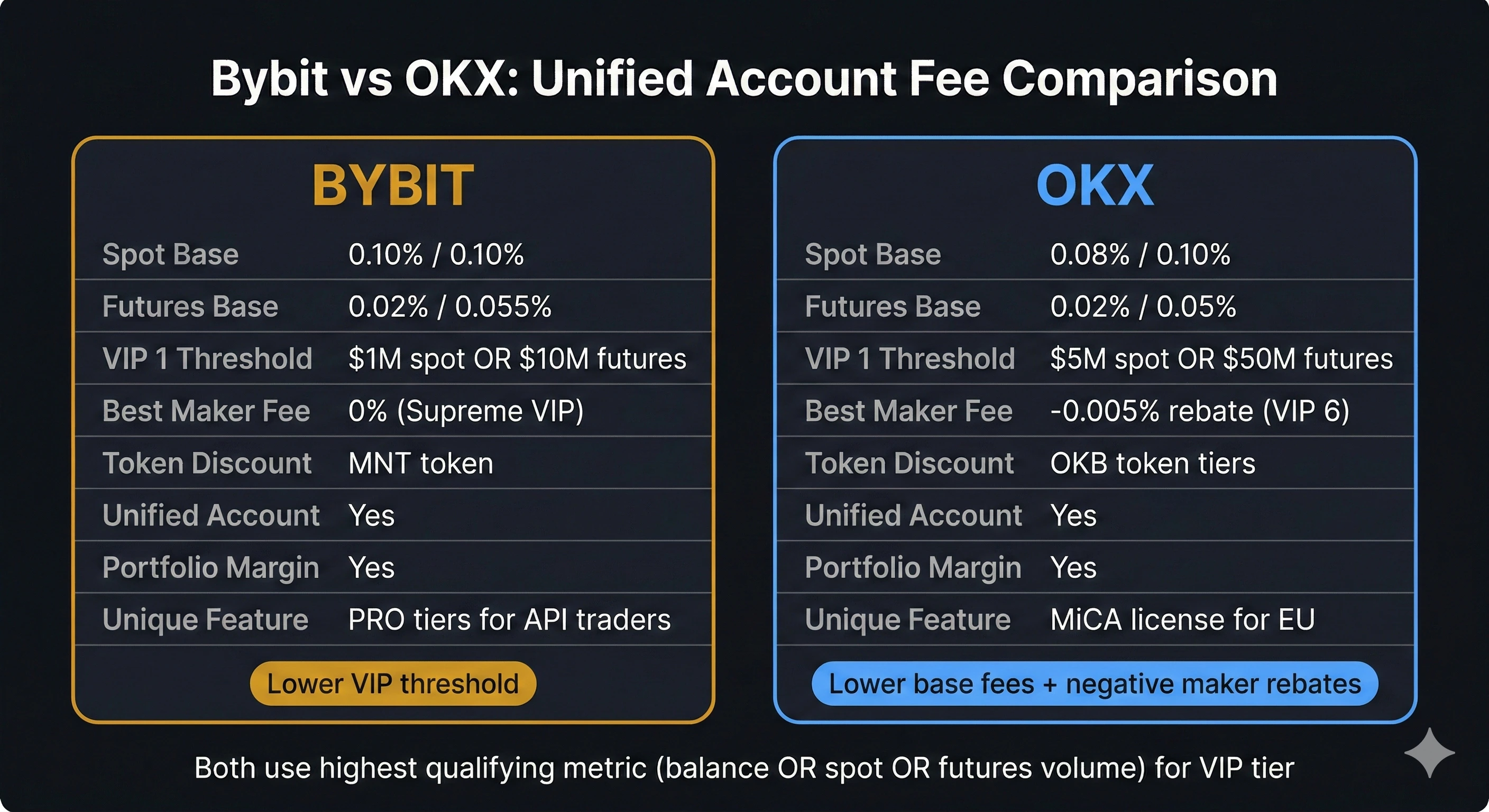

\n\n#4 and #5. Bybit and OKX — Unified Accounts and Portfolio Margin

\n\nBybit and OKX occupy similar territory: both are top-5 derivatives exchanges with unified trading accounts, competitive fee tiers, and strong API infrastructure. I'm covering them together because their fee structures are nearly identical at base tier, and the real differentiator is account architecture rather than cost.

\n\nBybit — Battle-Tested Derivatives With Unified Account

\n\n\n\nBybit's Unified Trading Account (UTA) is the feature that sets it apart. Instead of managing separate wallets for spot, derivatives, and options, UTA pools all your collateral into a single margin pool. This means unrealized profits on a winning BTC long can serve as margin for an ETH short—eliminating the capital inefficiency of transferring between sub-accounts. For multi-leg traders, this alone can save more than any fee discount.

\n\nThe base fee structure is standard: 0.10% / 0.10% on spot, 0.02% / 0.055% on perpetual futures. The VIP tier system is volume-based with MNT token holdings as a secondary qualifier. VIP 1 kicks in at $1M monthly volume, dropping futures taker to 0.04%. At the Supreme tier ($100B+ volume), maker hits 0% and taker drops to 0.018%—though this is institutional-only territory.

\n\nBybit currently lists 400+ spot assets and 450+ futures pairs, making it one of the broadest derivatives venues after Binance. The API is solid for automated trading, though during the February 2025 hack—where $1.5 billion was stolen from Bybit's cold storage in the largest single exchange theft in crypto history—API access experienced intermittent disruptions for roughly 12 hours. Bybit covered all losses from reserves without socializing them to users, which is worth noting as a trust signal, but the incident exposed serious operational security gaps.

\n\nRegulatory access has improved: the UK ban was lifted in December 2025, though US residents remain blocked. KYC is mandatory for all accounts.

\n\nBybit Fee Schedule — Key Tiers

\n\n| Tier | 30d Volume (USD) | Spot Maker/Taker | Futures Maker/Taker |

|---|---|---|---|

| Regular | <$1M | 0.10% / 0.10% | 0.02% / 0.055% |

| VIP 1 | ≥$1M | 0.06% / 0.08% | 0.018% / 0.04% |

| VIP 3 | ≥$25M | 0.04% / 0.06% | 0.014% / 0.032% |

| VIP 5 | ≥$300M | 0.02% / 0.04% | 0.010% / 0.024% |

| Supreme | ≥$100B | 0.005% / 0.02% | 0% / 0.018% |

Source: Bybit Official Fee Structure, verified March 2026.

\n\nPros and Cons

\n\n\n\n\n

\n\n\n\nPros

\n- \n

- Unified Trading Account pools margin across spot, futures, and options \n

- 450+ futures pairs — one of the broadest derivatives selections \n

- Competitive base futures fees (0.02% maker) \n

- Covered $1.5B hack losses from reserves without user socialization \n

- UK access restored (December 2025) \n

- Portfolio margin available for qualified accounts — significantly improves capital efficiency \n

Cons

\n- \n

- Suffered the largest exchange hack in crypto history ($1.5B, February 2025) \n

- Mandatory KYC — no anonymous trading \n

- Not available to US residents \n

- Spot taker fee (0.10%) tied with Binance, but Binance offers BNB discount to go lower \n

- VIP tier volume requirements are steep for retail traders \n

\n\n

\n\nOKX — Best Unified Margin and Token-Based Fee Optimization

\n\n\n\nOKX's unified account predates Bybit's and remains arguably the most sophisticated margin system in crypto. It supports cross-margin across spot, perpetuals, futures, and options in a single account with real-time portfolio risk calculation. The practical edge: if you're running a delta-neutral strategy with spot BTC as collateral backing a short perp position, OKX recognizes the hedged risk and requires substantially less margin than exchanges that evaluate each position independently.

\n\nThe fee structure starts at 0.08% / 0.10% for spot (slightly cheaper than Binance and Bybit) and 0.02% / 0.05% for futures. OKB token holders unlock tiered discounts, and at VIP 5 level ($100M+ monthly volume + OKB holdings), spot maker fees hit 0%. The OKB discount structure is more granular than Binance's flat BNB percentage—it's integrated into the VIP tier system rather than applied as a separate toggle.

\n\nOKX has also positioned itself aggressively in the on-chain space with its OKX Web3 wallet, which lets you trade across DEXs and bridge assets without leaving the OKX ecosystem. For traders who operate across both CEX and DEX venues, this reduces bridge friction and consolidates your trading activity.

\n\nOn the regulatory front, OKX holds licenses in Dubai (VARA), the Bahamas, and has applied for MiCA compliance in the EU. It exited the US and Canadian markets, so access is restricted for those jurisdictions.

\n\nOKX Fee Schedule — Key Tiers

\n\n| Tier | 30d Volume or OKB Balance | Spot Maker/Taker | Futures Maker/Taker |

|---|---|---|---|

| Regular | <$1M or <100 OKB | 0.08% / 0.10% | 0.02% / 0.05% |

| VIP 1 | ≥$1M or ≥500 OKB | 0.06% / 0.08% | 0.015% / 0.04% |

| VIP 3 | ≥$20M or ≥2,000 OKB | 0.04% / 0.06% | 0.010% / 0.028% |

| VIP 5 | ≥$100M or ≥5,000 OKB | 0% / 0.03% | 0.005% / 0.02% |

| VIP 8 | ≥$5B | -0.005% / 0.015% | 0% / 0.015% |

Source: OKX Official Fee and Rate Tiers, verified March 2026.

\n\nPros and Cons

\n\n\n\n\n

\n\n\n\nPros

\n- \n

- Most sophisticated unified margin system — true portfolio-level risk calculation \n

- Spot maker fees reach 0% at VIP 5, with maker rebates at VIP 8 \n

- Lower base spot fees (0.08%) than Binance and Bybit \n

- OKB token tiers provide an alternative path to fee reduction without volume \n

- Built-in Web3 wallet bridges CEX and DEX trading seamlessly \n

- Multi-jurisdiction licensing (VARA Dubai, Bahamas, MiCA pending) \n

Cons

\n- \n

- Not available in the US or Canada \n

- OKB-based tier requirements add token holding risk (OKB price exposure) \n

- Liquidity depth trails Binance on most pairs by 30-50% \n

- Historical association with OKEx brand and prior regulatory issues in China \n

- Customer support quality is inconsistent outside VIP tiers \n

\n\n

\n\n \n

\n#6. Decentralized Perps: dYdX v4 and Hyperliquid

\n\nDecentralized perpetual exchanges eliminate the custodial risk that haunts CEXs—you trade from your own wallet, and no centralized entity holds your collateral. After Bybit lost $1.5 billion in a single hack in February 2025, the case for self-custody trading infrastructure became harder to dismiss. But DEX perps come with their own cost profile: lower explicit fees offset by thinner liquidity, smart contract risk, and bridge friction.

\n\nThe two dominant platforms in this space are dYdX v4 (an appchain built on Cosmos) and Hyperliquid (a custom Layer-1 with its own consensus mechanism). Together they account for roughly 70-80% of all DEX perpetual futures volume. Their fee models are structurally different from CEXs and worth understanding separately.

\n\ndYdX v4 — The Only Exchange That Pays You to Trade

\n\n\n\ndYdX v4 migrated from Ethereum to a sovereign Cosmos-based appchain (dYdX Chain) in late 2023, which means it runs its own validators and matching engine rather than posting transactions to a general-purpose L1. The practical result: zero gas fees for trading, sub-second finality, and an off-chain order book that feels closer to a CEX than a typical AMM-based DEX.

\n\nThe fee structure is where dYdX stands apart. Base taker fees are 0.05%, but maker fees are negative: −0.011%. That's a rebate—you earn 1.1 bps on every filled maker order. For the momentum scalping example from earlier in this guide, this transforms the math entirely: your round-trip cost on a maker-entry/maker-exit trade is actually negative. The exchange pays you to provide liquidity.

\n\nOn top of the base rebate, dYdX runs a rewards program (branded "Surge") that distributes DYDX tokens to active traders. At certain volume tiers, the effective rebate can approach 50% of taker fees paid. The catch: reward programs are ephemeral. They can be reduced or eliminated by governance vote, so never build a trading system that depends on token rewards for profitability.

\n\ndYdX v4 Fee Schedule

\n\n| Tier | 30d Volume (USD) | Maker Fee | Taker Fee |

|---|---|---|---|

| 1 | <$1M | −0.011% | 0.050% |

| 2 | ≥$1M | −0.011% | 0.045% |

| 3 | ≥$5M | −0.011% | 0.040% |

| 4 | ≥$25M | −0.025% | 0.035% |

| 5 | ≥$125M | −0.025% | 0.030% |

Source: dYdX Official Fee Documentation, verified March 2026.

\n\nPros and Cons

\n\n\n\n\n

\n\n\n\nPros

\n- \n

- Negative maker fees (−0.011% rebate) — genuinely pays you to provide liquidity \n

- Zero gas fees for trading on the dYdX Chain \n

- Self-custodial: no exchange holds your funds \n

- Surge rewards program adds additional trading rebates \n

- DYDX staking provides further fee discounts \n

- Governance is genuinely decentralized via on-chain voting \n

Cons

\n- \n

- Order book depth significantly thinner than Binance — expect 3-5x more slippage on $500K+ orders \n

- Bridge friction: moving funds to dYdX Chain adds time and costs \n

- Limited pairs compared to CEXs (major assets only) \n

- Reward programs can be changed or discontinued via governance \n

- No spot trading — perpetual futures only \n

Hyperliquid — Fastest DEX With CEX-Level Performance

\n\n\n\nHyperliquid runs its own Layer-1 blockchain (HyperBFT consensus, not a fork) with sub-second finality and zero gas fees for trading. The matching engine handles approximately 20,000 orders per second in practice—not the 100,000 TPS marketing figure, but still fast enough that the trading experience feels indistinguishable from a centralized exchange. It dominated DEX perpetual futures in 2025, holding 60-80% market share and processing over $2.6 trillion in annual volume with just 11 employees.

\n\nThe fee structure is competitive but not as aggressive as dYdX's maker rebate: 0.015% maker / 0.045% taker on perpetuals, with higher rates on spot (0.04% / 0.07%). HYPE token staking provides discounts up to 40% off base fees. Where Hyperliquid genuinely excels is liquidity depth—in January 2026, it briefly surpassed Binance in BTC perpetual spread tightness ($1 vs. $5.50), though this fluctuates.

\n\nThe elephant in the room: security. Hyperliquid experienced three notable exploitation incidents in 2025, including a validator-level intervention to roll back a manipulated JELLY token position that highlighted the platform's centralization risks. The North Korean Lazarus Group was identified as having moved funds through Hyperliquid wallets, though the platform itself wasn't compromised. For a protocol that markets decentralization, the ability for validators to unilaterally reverse trades is a significant trust assumption that traders should understand.

\n\nHyperliquid Fee Schedule

\n\n| Market | Maker Fee | Taker Fee | HYPE Staking Discount |

|---|---|---|---|

| Perpetual Futures | 0.015% | 0.045% | Up to 40% off |

| Spot | 0.040% | 0.070% | Up to 40% off |

Source: Hyperliquid Official Fee Documentation, verified March 2026.

\n\nPros and Cons

\n\n\n\n\n

\n\n\n\nPros

\n- \n

- CEX-level execution speed with self-custody — the best UX in DEX perps \n

- Zero gas fees for trading \n

- Deep liquidity on major pairs — competitive with top CEXs on BTC/ETH \n

- No KYC required (IP-based geofencing only) \n

- HYPE staking discounts stack meaningfully (up to 40%) \n

- Spot trading available alongside perpetuals \n

Cons

\n- \n

- Validators intervened to reverse trades during the JELLY incident — centralization risk \n

- Three manipulation/exploitation events in 2025 raise security concerns \n

- Max leverage capped at 50x on majors — lower than CEX competitors \n

- Geofenced for US, Russia, and sanctioned regions (VPN use is ToS violation) \n

- HYPE token down ~50% from ATH — staking economics depend on token price stability \n

- 37-minute outage in July 2025 exposed capacity limits under stress \n

DEX vs CEX: When Do the Fee Savings Actually Matter?

\n\nThe fee comparison between DEX and CEX perps isn't as straightforward as comparing percentages. dYdX's −0.011% maker rebate looks unbeatable, but if your $200K order experiences 5 bps more slippage than it would on Binance due to thinner depth, you've lost more than the rebate saved you. Hyperliquid's liquidity is approaching CEX levels on BTC and ETH, but on altcoin perps the depth difference is still substantial.

\n\nThe real calculus involves three variables: explicit fees (where DEXs win), slippage (where CEXs typically win), and custodial risk (where DEXs win decisively after the Bybit hack). For traders executing under $50K per order on major pairs, DEX perps are now genuinely competitive on total cost. For larger orders or altcoin positions, CEX liquidity still justifies the custody tradeoff for most traders.

\n\n\n\nBitget Fees: Standard Spot and USDT Perpetual Rates (2026)

\n\nBitget charges 0.10% maker and 0.10% taker on spot, and 0.020% maker / 0.060% taker on USDT perpetual futures at the standard tier. That spot rate is mid-pack, but the futures maker fee is among the more competitive on this list, which matters if you post liquidity on perps. Holding BGB (Bitget's exchange token) applies a 20% discount, dropping spot to 0.08% maker/taker, and 30-day volume tiers reduce it further.

\n\nFor a maker-heavy futures strategy, Bitget's 0.020% maker matches Binance's standard 0.020%, but it undercuts most retail spot venues on the taker side once BGB is applied. As always, the fee you actually pay is your tier rate minus token and volume discounts, not the headline number.

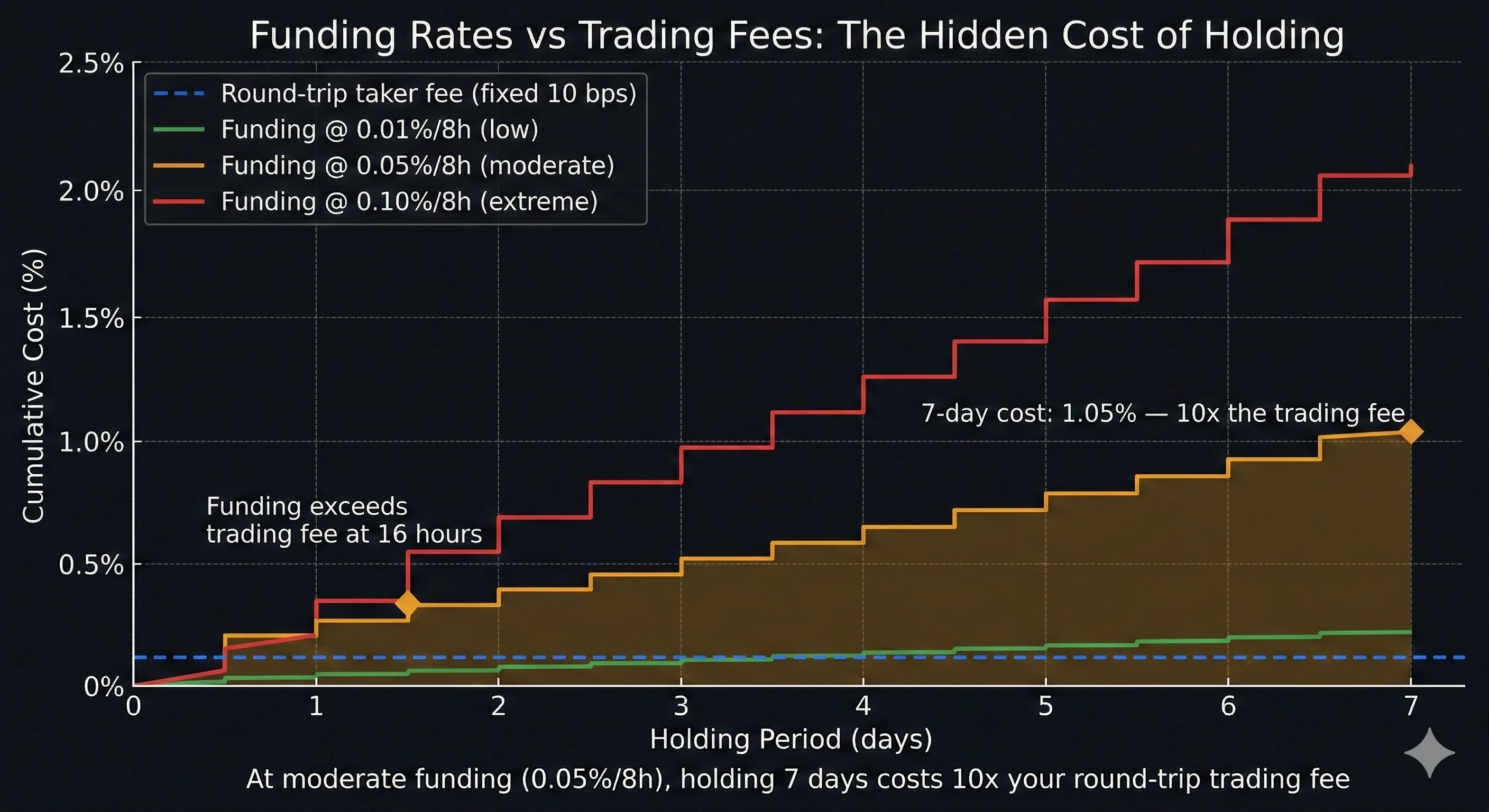

\n\nHow Do Funding Rates Compare to Trading Fees?

\n\nIf you trade perpetual futures and hold positions for more than a few hours, funding rates will almost certainly cost you more than the maker/taker fee. This is the most underappreciated cost in crypto derivatives, and it's the reason many "profitable" swing trading systems quietly bleed money.

Funding payments you receive are also taxable income, and the way your tax software buckets them matters at filing time. See how crypto futures funding rates and prop firm payouts are taxed in 2026 for the reporting rules and the software that gets it right.

\n\nHow Perpetual Futures Funding Rates Work

\n\nPerpetual futures have no expiration date, so exchanges use a funding rate mechanism to keep the contract price anchored to the spot index. Every 8 hours on most exchanges (Binance, Bybit, OKX) or every 1 hour on Hyperliquid, longs pay shorts (when funding is positive) or shorts pay longs (when funding is negative). The rate is determined by the premium/discount of the perp price relative to spot and the prevailing interest rate differential.

\n\nDuring trending bull markets, funding rates on BTC perpetuals routinely hit 0.01% to 0.03% per 8-hour interval. That doesn't sound like much—until you compound it. At 0.02% per interval, a long position held for 3 days pays 0.18% in funding (9 intervals × 0.02%). That's equivalent to 18 bps—which is 3.6x more expensive than a round-trip taker trade on Binance at 0.05% per side.

\n\nThe Cost Comparison: Fee vs Funding Over Time

\n\nLet's put concrete numbers on this for a $100,000 BTC perpetual long position on Binance:

\n\n| Holding Period | Trading Fee (Taker RT) | Funding Cost (at 0.02%/8h) | Total Cost | Which Costs More? |

|---|---|---|---|---|

| 1 trade (scalp) | $100 (10 bps) | $0 | $100 | Trading fee |

| 8 hours | $100 | $20 (2 bps) | $120 | Trading fee |

| 24 hours | $100 | $60 (6 bps) | $160 | Trading fee |

| 3 days | $100 | $180 (18 bps) | $280 | Funding (1.8x) |

| 7 days | $100 | $420 (42 bps) | $520 | Funding (4.2x) |

| 30 days | $100 | $1,800 (180 bps) | $1,900 | Funding (18x) |

The crossover point is roughly 10-12 hours at typical funding rates. Beyond that, funding dominates your total cost. During extreme sentiment (like the bull runs of early 2025), funding rates spiked to 0.05%-0.10% per interval, which means holding a long for a single day could cost more than 10 round-trip trades in fees.

\n\nStrategies to Minimize Funding Rate Costs

\n\nMonitor before entering: Always check the current funding rate and next predicted funding on your exchange before opening a perpetual position. On Binance, this is displayed directly on the trading interface. If funding is abnormally high (above 0.03%), consider whether your position thesis justifies the carrying cost.

\n\nTime your entries around settlements: Funding is charged at settlement time (00:00, 08:00, 16:00 UTC on Binance). If you're opening a short-duration position, entering right after a settlement and exiting before the next one means you pay zero funding. This is free optimization that costs nothing to implement.

\n\nUse quarterly futures instead: Traditional dated futures (available on Binance, OKX, and Bybit) have no funding rate. The premium or discount is baked into the price and converges to zero at expiry. For positions held longer than 48 hours, quarterly futures are almost always cheaper than perpetuals. The tradeoff is less liquidity and the need to roll positions near expiration.

\n\nCollect funding with delta-neutral strategies: When funding is persistently positive, experienced traders go long spot BTC and short the perpetual of equal size. The position is market-neutral (you profit $0 from price movement) but you collect the funding payment every 8 hours. This is essentially a carry trade—your return is the funding rate minus the cost of capital and trading fees. On Binance with maker orders, the round-trip cost is 4 bps, so any daily funding above ~1.5 bps per interval makes this profitable.

\n\n\n\n \n

\nWhich Exchange Should You Use Based on Your Trading Style?

\n\nThe "best" exchange depends entirely on how you trade. A scalper optimizing for 5 bps needs a fundamentally different venue than a swing trader holding positions for weeks. Here's the decision matrix based on real cost analysis, not marketing claims.

\n\nHigh-Frequency Scalpers (10+ Trades Per Day, <20 bps Targets)

\n\nPrimary: MEXC (0% maker) | Secondary: dYdX v4 (−0.011% maker rebate)

\n\nWhen your gross profit target is under 20 bps per trade, every basis point of fee is existential. The EV decay formula from earlier in this guide proves it: at 10 bps round-trip fees, a 60% win-rate / 15 bps target system becomes a guaranteed loser. MEXC's 0% maker fee eliminates this problem entirely for maker-to-maker strategies. dYdX's negative maker fee actually adds to your edge.

\n\nThe caveat: both platforms have thinner liquidity than Binance on most pairs. If you're scalping anything beyond BTC/USDT and ETH/USDT, verify the order book depth before committing. A 0% fee means nothing if you're paying 10 bps in spread to enter and exit.

\n\nActive Day Traders (3-10 Trades Per Day, 20-100 bps Targets)

\n\nPrimary: Binance | Secondary: OKX

\n\nFor day traders with wider targets, the fee percentage matters less than total execution cost. Binance's unmatched liquidity depth means consistently tighter spreads and less slippage—which compounds across hundreds of trades per month. The 0.02% futures maker fee with BNB discount (effective 0.018%) is competitive enough that the liquidity advantage makes Binance the rational choice.

\n\nOKX is the strong alternative if you trade multiple asset classes simultaneously. The unified margin system lets a profitable spot position reduce your futures margin requirements in real-time, improving capital efficiency by 20-40% for multi-leg strategies.

\n\nSwing Traders (Holding 1-14 Days)

\n\nPrimary: Binance (quarterly futures) | Secondary: Bybit (UTA)

\n\nFor swing traders, trading fees are a one-time cost but funding rates compound every 8 hours. The section above on funding rates shows that a 3-day hold at typical funding rates costs 18 bps—nearly double a taker round-trip. Use quarterly futures instead of perpetuals to eliminate funding entirely. Binance offers the deepest quarterly futures liquidity.

\n\nBybit's Unified Trading Account is valuable here because your unrealized spot gains collateralize your futures positions without manual transfers—useful when managing correlated swing positions across multiple assets.

\n\nEU-Based Traders Prioritizing Fiat Rails

\n\nPrimary: Kraken Pro | Secondary: Binance (MiCA-pending)

\n\nIf you're depositing and withdrawing in EUR, Kraken's SEPA Instant integration is unmatched. Deposits arrive in seconds, and the EUR/crypto pairs have competitive liquidity for European trading hours. The higher base spot fees (0.25% / 0.40%) are offset by the zero-friction fiat experience and full regulatory compliance. Volume tiers drop maker to 0% at $10M+ monthly.

\n\nBinance is working toward MiCA compliance but the regulatory status varies by EU member state. For traders who need guaranteed access with a regulated EU entity, Kraken is the safer choice today.

\n\nSelf-Custody Maximalists (No CEX Trust)

\n\nPrimary: Hyperliquid (best UX) | Secondary: dYdX v4 (best maker economics)

\n\nAfter $1.5 billion vanished from Bybit's cold storage in a single attack, the "not your keys, not your crypto" argument carries real financial weight. Both Hyperliquid and dYdX let you trade perpetuals from your own wallet without depositing funds into a centralized custodian.

\n\nHyperliquid wins on user experience and liquidity depth. dYdX wins on maker fee economics. Neither matches CEX depth on altcoin pairs. If you're exclusively trading BTC and ETH perps and refuse to trust a centralized exchange, these are viable primary venues.

\n\n\n\n\n\nWhat Are the Most Common Fee Mistakes Crypto Traders Make?

\n\nAfter reviewing my own trading logs and talking to dozens of traders in prop firm communities, the same fee mistakes come up repeatedly. Most of them are easy to fix once you know they exist—but they can silently drain thousands of dollars per month from traders who never audit their execution costs.

\n\nMistake #1: Assuming All Limit Orders Are Maker Orders

\n\nThis is the most expensive misconception in crypto trading. A limit buy at $60,050 when the best ask is $60,000 executes immediately as a taker order. You pay taker fees despite using a "limit" order. The fix is simple: use the Post-Only flag on every order where you need guaranteed maker classification. I covered this in the order types section—if you skipped it, go back and read it.

\n\nI've seen traders run automated systems for months without realizing every single order was crossing the spread and paying taker fees. One look at the "Fee Type" column in their trade history would have revealed it immediately.

\n\nMistake #2: Choosing an Exchange Based Solely on the Lowest Fee Percentage

\n\nMEXC's 0% maker fee looks unbeatable on a comparison table. But if you're trading a low-cap altcoin with a 40 bps spread on MEXC versus a 5 bps spread on Binance, you're paying 35 bps more in implicit costs to "save" 2 bps in explicit fees. Always evaluate total execution cost: explicit fee + spread + slippage. The Transaction Cost Analysis section above provides the complete framework.

\n\nThe rule of thumb: for BTC and ETH on major exchanges, explicit fees dominate total cost. For altcoins below the top 50 by market cap, spread and slippage dominate. Route accordingly.

\n\nMistake #3: Not Enabling Native Token Fee Discounts

\n\nBinance gives you a 25% spot fee discount for paying fees in BNB. It's a single toggle in your settings. Yet I've met traders with $50K+ monthly volume who never activated it because they didn't know it existed. OKX and Bybit have similar token-based discount mechanisms. The setup takes 60 seconds and saves real money across every trade you execute.

\n\nThe checklist: hold a small balance of BNB (Binance), MNT (Bybit), OKB (OKX), or MX (MEXC) and enable the fee deduction setting. On Binance specifically, note that the BNB futures discount is 10%, not 25%—a common source of confusion.

\n\nMistake #4: Ignoring Funding Rates on Perpetual Futures

\n\nCovered extensively in the funding rates section, but it bears repeating here: traders who hold perpetual futures positions for days or weeks while obsessing over saving 2 bps on trading fees are optimizing the wrong variable. Funding rates during trending markets can exceed 100 bps per day. Check funding before every entry, and use quarterly futures for any position you plan to hold longer than 24 hours.

\n\nMistake #5: Using Stop-Market Orders as Default Stop-Losses

\n\nStop-market orders guarantee execution but guarantee taker fees and, in thin liquidity, severe slippage. During a cascading liquidation event, a stop-market at $60,000 might fill at $59,800 after sweeping through a depleted order book. That 200 bps of slippage dwarfs any fee optimization you've done.

\n\nThe alternative: use stop-limit orders with a limit price offset from your stop trigger. Set the stop at $60,000 and the limit sell at $60,100—the order rests on the book as a maker. The risk is non-execution if the market gaps through your limit, so only use this approach for situations where partial fill risk is acceptable. For genuine emergency exits, stop-market is correct—just understand the cost.

\n\nMistake #6: Never Auditing Your Actual Fee Classification

\n\nEvery exchange provides a trade history export with fee classifications. Download yours and check what percentage of your orders are actually receiving maker fees versus taker fees. If you're running a strategy that should be 90% maker and you discover 40% of fills are taker (due to spread volatility, timing issues, or missing Post-Only flags), you've found a direct optimization worth hundreds or thousands of dollars per month.

\n\nOn Binance, go to Orders → Trade History → Export. The CSV includes a "Fee" and "Role" column. On Bybit and OKX, the equivalent export is under Transaction History. Run this audit monthly.

\n\nMistake #7: Trading on the Wrong Venue for Your Order Size

\n\nA $500 order on Binance and a $500 order on Hyperliquid have nearly identical execution quality. A $500,000 order is a completely different story. Order book depth varies dramatically across exchanges and pairs. Before routing large orders, check the depth at ±5 bps from the mid-price. If your order exceeds 20% of the resting liquidity at your price level, you're guaranteed to pay significant market impact—and you should either split the order with a TWAP algorithm or route to a deeper venue.

\n\n\n\nFrequently Asked Questions

\n\nWhat is the difference between a maker and a taker fee in crypto?

A maker fee is charged when your order rests on the order book and waits to be filled — you're adding liquidity. A taker fee is charged when your order matches immediately against existing orders — you're removing liquidity. Maker fees are lower (or even negative as rebates) because exchanges incentivize deeper order books. The classification depends on execution behavior, not order type: a limit order that crosses the spread pays taker fees.

Can a limit order be charged taker fees?

Yes. If you place a limit buy at $60,050 when the best ask is $60,000, your order matches immediately and you pay taker fees despite using a limit order. To guarantee maker classification, use the Post-Only flag — it cancels your order instead of executing it as a taker.

Which crypto exchange has the lowest trading fees in 2026?

MEXC offers the lowest base fees: 0% maker on both spot and futures, with 0.02% taker on futures and 0.05% taker on spot. However, "lowest fees" doesn't mean "lowest cost." Binance and OKX have significantly deeper liquidity, meaning tighter spreads and less slippage — which often matters more than the explicit fee percentage, especially for orders above $10,000.

How do I calculate my breakeven price including trading fees?

For a long position: Breakeven = Entry Price × (1 + Entry Fee) / (1 − Exit Fee). For example, entering long at $100,000 with 0.04% fees on both legs means you need Bitcoin to reach $100,080 just to break even. With leverage, fees are calculated on the full notional position size, not your margin deposit.

What is a Post-Only order and why should I use it?

A Post-Only order instructs the exchange to only accept your order if it will rest on the order book as a maker. If the order would cross the spread and execute immediately (becoming a taker), it gets cancelled instead. This guarantees you pay maker fees and prevents accidental taker fills during volatile spreads. Available on Binance, Bybit, Kraken, OKX, dYdX, and Hyperliquid.

Are funding rates more important than trading fees for perpetual futures?

For positions held longer than a few hours, funding rates typically dwarf trading fees. Funding settles every 8 hours on most exchanges and can run 0.01% to 0.03% per interval during trending markets. A position held for 3 days during high positive funding could pay 0.09% to 0.27% — far more than a 0.05% taker fee. Always check the current funding rate before entering a perpetual futures position.

Do VIP tiers actually save significant money?

For most retail traders, VIP tiers are unreachable. Binance VIP 1 requires $1M in 30-day volume plus 25 BNB. The real savings come from simpler optimizations: enabling BNB fee deduction on Binance (instant 25% spot discount), holding 500 MX on MEXC (50% off), or using Post-Only orders to avoid taker fees entirely. These moves save more than chasing VIP status for 95% of traders.

Should I use dYdX or Hyperliquid to save on fees?

Both offer competitive fee structures for derivatives. dYdX v4 provides a −0.011% maker rebate (you earn money providing liquidity) with 0.05% base taker fees, plus 50% trading rebates through their rewards program. Hyperliquid charges 0.015% maker / 0.045% taker on perps with HYPE staking discounts up to 40%. The tradeoff is liquidity depth: neither matches Binance's order book depth on major pairs, so slippage on larger orders may offset the fee savings.

Final Verdict: Treat Fees as an Engineering Variable, Not a Fixed Cost

\n\n\n\n\nSources and Official Fee Schedules

\nAll fee data in this guide was verified against official exchange documentation as of March 2026. Fee schedules change frequently — always confirm current rates before trading.

\n- \n

- Binance — Official Fee Schedule \n

- Kraken — Fee Structure and Volume Tiers \n

- MEXC — Trading Fees \n

- Bybit — Trading Fee Structure \n

- OKX — Trading Fee and Rate Tiers \n

- dYdX — Trading Fees Documentation \n

- Hyperliquid — Fee Schedule and Staking Discounts \n

Regulatory References

\n- \n

- Regulation (EU) 2023/1114 — Markets in Crypto-Assets (MiCA) — EUR-Lex full text \n

- ESMA — MiCA Implementation and Register \n

Educational References

\n\n\n

Disclosure: This guide contains affiliate links. If you sign up through them, we may earn a commission at no extra cost to you. This doesn't influence our recommendations—see our editorial policy.

\nMore Guides

8 Books You Need to Read Before You Start Trading

Eight books that build the mindset, chart skills, and habits to have before you risk real money on your first trade.

Best Crypto Exchanges 2026: Fees, Safety & Honest Reviews

Compare 12 crypto exchanges with verified fees, security records, and trust ratings. Includes scam warnings, corrected data, and the 2026 regulatory shift.

How to File Crypto Futures and Prop Firm Taxes in 2026: Best Software Compared

Filing taxes on perpetual futures, funding rates, and prop firm payouts is a nightmare most crypto tax guides ignore. This guide breaks down exactly how BTC futures and funded trading income gets taxed in 2026, which IRS forms you need, and which tax software actually handles it.

How to Start Scalp Trading as a Beginner in 2026 (Complete Guide)

Master scalp trading with this complete 2026 guide. Learn order flow analysis, AAA setups, value area trading, risk management, and professional execution strategies.

Trading Survival Guide 2026: Risk, Position Sizing & Discipline

Master trading in 2026 with proven strategies for risk management, position sizing, and emotional discipline. Learn the essential 2:1 risk-reward rule.

Kinsta WordPress Hosting in 2026: Built for Speed (and Your First Month Free)

Kinsta runs WordPress on Google Cloud premium-tier C2 instances with server-level NGINX caching and bundled Cloudflare Enterprise CDN. Sub-200ms TTFB consistently, Core Web Vitals built in, plus the first month free on Single 35k and WP 2 plans.

8 Books You Need to Read Before You Start Trading

Eight books that build the mindset, chart skills, and habits to have before you risk real money on your first trade.

Read next in Guides →